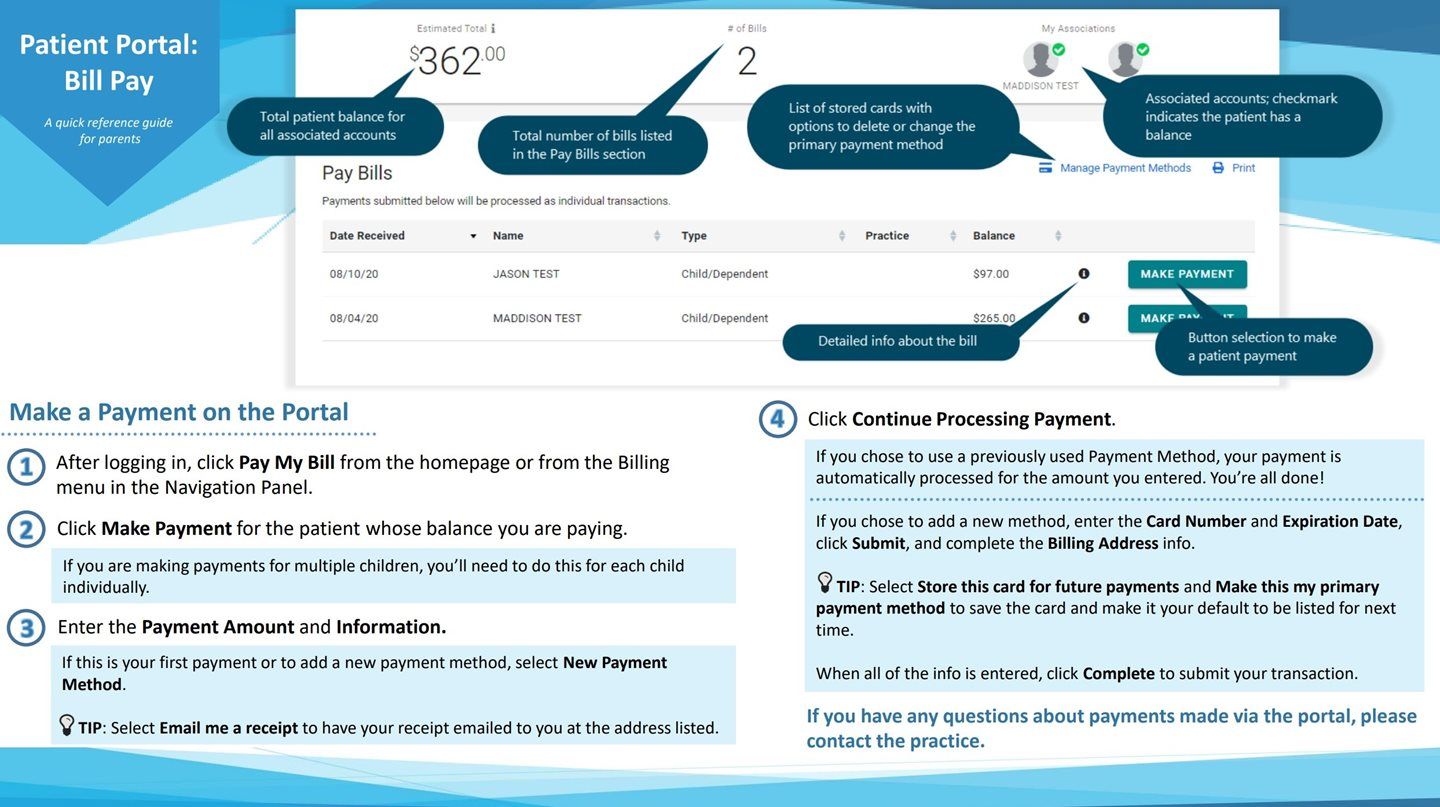

Insurance & Billing

Billing staff

We have our own billing staff and they are happy to help you understand your bills and develop a payment plan if needed.

You can find their number at the top of this site. It is 913-825-0923

Healthcare Information

- Take Healthcare into your own hands: HealthCare.gov

- Kansas healthcare information: Kansas Insurance Department

- Health Reform: Daily Reports from Kaiser Health News

- Health Reform and Updates from the Kansas American Academy of Pediatrics

Insurance

Understanding Your Insurance Plan

Many parents of our patients have questions regarding their insurance coverage of certain services. Our office accepts many plans; each is underwritten between a person’s employer and the insurance company, so even two Coventry contracts might be different. We are unable to know every patient’s specific plan.

Most insurance companies today share costs with the patient. There are many cost sharing options for you to choose, and we abide by the billing, coding, and collections set forth by your plan.

Formulary Information:

It is often important to learn the formulary drug status when choosing a medication to keep your costs low.

Our office receives many requests to change a prescription due to insurance cost, but usually we do not know what the preferred medication is. The insurance company provides its members with a formulary, usually available online to its customers but not to the general public (or doctors).

We cannot prescribe the cheapest medicine unless we know what your formulary is. That requires you to look up the medicines on the formulary. You will need to access your insurance company's website private portal to look up this information.

Deductible:

The total amount of covered medical expenses that must be paid by the patient before the insurance company begins paying benefits. After this requirement is reached, the insurer will begin paying according to terms of the contract — often 75-85% of covered medical costs. The patient is responsible for any remaining balance.

Flat-rate copayment:

The patient pays a share of covered medical costs and the insurance carrier pays an amount based on the policy. For example, when the patient pays $15 of any office visit charge or $3 for any prescription, the insurance carrier is responsible for the balance.

Percentage-based copayment:

The patient pays a percentage share of covered medical costs and the insurance company pays an amount based on the patient's policy. Examples: 20% of the office visit charge would be $10 of a $50 charge, $12 of a $60 charge, etc. Typically this copayment arrangement includes a deductible and may have other variations.

Consumer-driven health plans (CDHPs):

CDHPs are the fastest growing plan type currently across the county. Employers are shifting financial responsibility to their employees by offering health plans with high deductibles and coinsurance to reduce cost to the business. Most of these plans cover wellness services such as immunizations, well-child visits, and periodic check-ups more than sick services. They usually have a high deductible, but when the deductible is met, the plan pays for services at a percentage (such as 80%) of a defined reasonable and customary fee schedule.

Health savings accounts (HSAs):

HSAs are tax-favored savings accounts funded with pretax dollars by the individual or the employer. Money can be withdrawn from the account at any time with no penalty or taxes to pay for qualified medical expenses. An HSA can be established only along with high-deductible health insurance plans that meet Internal Revenue Service rules that set the amount of the individual and family deductible. The amount an employee can put in an HSA is capped at the amount of his or her annual deductible of his or her health insurance policy. Any unused funds each year remain in the account, accumulate tax-free and can be used for future medical expenses.

Health reimbursement accounts (HRAs):

HRAs are funded by the employer and can be used by an employee as pretax dollars. These accounts can be set up independent of any specific health plan or benefit design. Money can be used to pay for medical expenses. HRA funds can also be carried over from year to year. The amount of the contributions to the HRA varies based on the employer. The employer owns the fund and any unused amounts may or may not be transferred on termination of employment, depending on the terms of the fund. Medical spending accounts (MSAs) and flexible spending accounts (FSAs) are versions of HRAs with particular features.

Understand the fine print of your plan

Your health insurance policy is an agreement between you and your insurance company. It is generally negotiated by your employer if it is an employee benefit. The policy lists a package of medical benefits such as tests, medications, and treatment services. The insurance company agrees to cover the cost of certain benefits listed in your policy. These are called "covered services." Coverage does not guarantee full payment and your insurance company may require partial coverage by the policyholder. Your policy also lists the kinds of services that are not covered by your insurance company. You have to pay for any uncovered medical care that you receive.

Be aware that a medical necessity is not the same as a medical benefit. A medical necessity is something that your provider has decided is necessary based on clinical presentation and standard of care. A medical benefit is something that your insurance plan has agreed to cover. In some cases, your provider might decide that you need medical care that is not covered by your insurance policy. Common examples of this might be a splint for a sprain or a spacer device to use with an inhaler for wheezing.

Helpful Tips:

Since we are unable to know the specifics of every insurance plan, we encourage families to understand their own coverage. One would never buy a car without test driving several makes/models and making an informed choice. On the same token, we encourage families to read their insurance information to make an informed decision of which plan to choose (if more than one is offered by the employer). By understanding your insurance coverage, you can help your doctor recommend medical care that is covered in your plan.

- Take the time to read your insurance policy. It's better to know what your insurance company will pay for before you receive a service, get a lab or x-ray, or fill a prescription.

- Some medications, tests or hospitalizations may have to be approved by your insurance company before your doctor can provide them. Our office will charge if the prior authorization takes a significant amount of nursing time, but not if it is a simple form to fax.

- If you still have questions about your coverage, call your insurance company and ask a representative to explain it.

- Remember that your insurance company, not your provider or the physician's office, makes decisions about what will be paid for and what will not.

Vaccines for Children (Medicaid and no insurance)

Children without insurance and those with Medicaid insurance can get vaccines from the Vaccines For Children (VFC) program. Learn more here.

Frequently Asked Questions (FAQs):

Why am I charged at a well visit?

A preventive care visit (routine well visit) focuses on overall health and how to stay healthy. But a preventive visit may turn into an office visit that costs you money. Learn why.

When does a preventive visit become an office visit?

A preventive care visit is different from an office visit:

- The purpose of a preventive visit is to review your overall health, identify risks and find out how to stay healthy. Most insurance plans cover 100% of a preventive visit when you see a doctor in your plan network.

- The purpose of an office visit is to discuss or get treated for a specific health concern or condition. You may have to pay for the visit as part of your deductible, copay and/or coinsurance.

If you schedule a preventive care visit and ask about a specific health concern or condition, it may trigger an additional charge for an office visit.

If you want to know about costs, ask your insurance plan for an estimate of fees before you visit. You can call the number on the back of your member ID card and describe what you want to cover at your well visit. The table below shows what services are typically covered during a preventive visit.

What can I discuss at a preventive visit without getting charged?

During your preventive well care visit, the following is included:

- Your current health

- Your family health history

- Past illnesses and surgeries

- Risks you may have for specific conditions (note: some insurance companies deny coverage for the recommended screening surveys)

- How to maintain a healthy lifestyle

What is the difference between a preventive care visit and an office visit?

A Preventive Care Visit

Your plan typically covers these services

- Check your weight, height, blood pressure (over 3 years) and pulse

- Listen to your heart and lungs

- Check your ears, eyes, throat, skin and abdomen

- Recommended immunizations

- Screenings vary by age (development, lead, depression)

- Certain blood tests, such as to check for high cholesterol, lead or anemia

An Office Visit

You may be required to pay for these services, even if addressed during a preventative care visit

- Discussing or getting treatment for a specific health concern, condition or injury

- Refills of prescriptions are considered getting treatment for health conditions

- Lab work, X-rays or additional tests related to a specific health concern, condition or injury

Most of the things your provider recommends for routine preventative care will be covered by your plan, but some may not. This may include some of the screening recommendations and tests recommended routinely if your insurance company does not cover them. We will not know this in advance. It is insurance plan dependent.

When you have a test or treatment that isn't covered, or you get a prescription filled for a drug that isn't covered, your insurance company won't pay the bill. This is often called "denying the claim." You can still obtain the treatment that is recommended, but you will have to pay for it yourself. Some companies will pay a percentage and the patient is responsible for the remainder. This is in addition to your co-pay.

If your insurance company denies your claim, you have the right to appeal (challenge) the decision. Before you decide to appeal, know your insurance company's appeal process. This should be discussed in your plan handbook. Not all appeals will end in your favor, but some challenged claims will be covered eventually by the insurance company.

Most insurance companies have different levels of co-pays for the primary care office, specialist, urgent care, and emergency room. These are often printed on your insurance card and can change yearly with new contracts. Some insurance plans require a referral to see any provider other than your primary care provider on your insurance card.

Why does the front desk always ask for my card?

Bring your insurance card with you to each visit. Even if you have the same plan as last year, the copays might be different. Sometimes the insurance billing address has changed. We cannot file your claim properly without the correct information.

How do I know what medicines will be least expensive?

A formulary is a list of medications that your insurance company will help you pay for. It puts medications in two or three categories (tiers) based on co-pay. The first tier is usually generic medications, the second more expensive medications and the third the most expensive medications. Each tier has a higher copay.

This list is reviewed and changed by the insurance company every few months, so your cost might go up or down. Be aware of the formulary before you begin any medication, especially one that will continue long term. Learn if your insurance gives a discount for using their mail-in prescription service. Insurance companies, not the pharmacy, decide on the cost of the copay. They might contract with particular pharmacies and your cost will be lower at those pharmacies.

We are happy to write for prescriptions with lesser copays if they will treat the condition properly and you know your formulary. Because we see hundreds of plans and formularies change, we do not know what your plan prefers. We cannot continue to write new prescriptions until one is found that is least expensive, so please do not call the office multiple times for another medication because "this one is too expensive also." Know your formulary!

What if I have a question about a bill?

If you do not understand a bill or explanation of benefits (EOB), please call your benefits administrator or human resources administrator, or our office billing department.

What do I do if I received a bill that I don’t think I should have to pay?

Sometimes insurance companies believe that a test, procedure, or therapy is warranted, but they will not cover it and require the patient to pay. For example, our office has received several complaints from parents about the charge for the autism screen we recently started performing. In October 2007, the American Academy of Pediatrics initiated a new standard of care that all children at 18 and 24 months be screened for autism with a standardized test. Prior to this, our office asked screening questions for both motor and verbal development at each well check. According to the new guidelines, questions that are not part of a standardized evaluation are not sufficient. We chose to use the MCHAT (Modified Checklist for Autism in Toddlers) because of its ease of use, validity, and reliability.

We use numbered codes to submit services to insurance companies. These codes vary from the visit itself to diagnoses made and tests performed. We are encouraged to use codes for everything we do to document to the insurance company what care was given at a visit. Insurance companies use these codes to monitor practice patterns and optimum care. For instance, if a child with asthma does not fill a prescription for a controller (prevention) medicine, we may receive a letter of reprimand from their insurance company stating that we should prescribe one. In some cases we have written a prescription, but the family chooses to not fill it. In other cases, we do not feel that child meets criteria for daily medication. Either way, the insurance company “dings” us for poor compliance to standard of care.

When there is a new standard of care, such as the Autism screen, it takes time for the insurance companies to recognize the new code. Sometimes a company never pays on that code. Unfortunately, in order for us to provide the standard of care, which we strive to follow for all patients in all instances, we must provide this service and submit the code to the insurance companies. The service may seem minimal, but it does incur a cost to our business. With the MCHAT, we must print the forms, monitor inventory, ensure that each child at the appropriate age has a completed form, score the form, discuss results, and scan the form into the patient’s chart.

How can I help my insurance company begin to cover costs of currently allowable but not covered bene

We encourage parents to call their insurance companies and talk with their Human Resources personnel to discuss billing disputes. When insurance companies review the concerns of consumers, they may change policies. Also, class action lawsuits against insurance companies sometimes force payments. The MCHAT example above can be continued in this line. Information provided by the AAP as well as compliance disputes filed by several pediatricians were instrumental in impacting CIGNA’s decision to rescind its practice of bundling payments for developmental screening. Per Deborah Winegard, Legal Counsel for the California Medical Association (and formerly the Compliance Dispute Facilitator for the CIGNA managed care settlement agreement), effective May 1, 2008, CIGNA began paying physicians who bill properly for developmental screening. Payments will be made on all bills submitted after May 1 regardless of date of service. Although the settlement has ended, CIGNA has agreed to make this payment change on a going forward basis. Settlement agreements with Aetna, HealthNet, Humana, WellPoint, and the Blue Cross/Clue Shield Association remain in effect.

If your insurance company is one that does not recognize the value in any service (whether it is this screen or any other medically indicated service), please call your insurance representative to demand coverage for recommended services. Every call they receive may or may not immediately change their benefits, but if enough concern is raised with a particular issue, there is a better chance it will at least be discussed.

Talk to our business office about any billing disputes

Thank you to all the families who did call to let us know a problem existed with the MCHAT, the new mandated service described above. As always, if you do have a concern, please let our office know. That is how we know what is happening with our patient families. We do care and would like to offer any help we can with any issues that arise.

Key Insurance Terms:

Billing Statement:

A summary of current activity on an account.

Birthday Rule:

To determine which parent carries primary insurance and which will be secondary if both parents will cover insurance, a birthday rule is generally accepted. Under this rule, the plan of the parent whose birthday occurs first in the calendar year is designated as primary. The date of birth is the determining factor — not the year — so it doesn't matter which spouse is older. Like most rules, the birthday rule has exceptions:

- If both parents share the same birthday, the parent who has been covered by his or her plan longest provides the primary coverage for the children.

- If one spouse is currently employed and has health insurance through a current employer, and the other spouse has coverage through a former employer (e.g., through COBRA), the plan belonging to the currently employed spouse would be primary.

- In the event of divorce or separation, the plan of the parent with custody generally provides primary coverage. If the custodial parent remarries, the new spouse's coverage becomes secondary. And finally, the non-custodial parent's plan would provide a third layer of insurance protection. This order of payment can be altered by a court-issued divorce decree or by agreement, but the insurance companies must be notified.

Claim:

Information billed to the insurance company for services provided.

Co-payment or Co-Insurance:

The balance due by the policyholder as determined by the insurance company.

Deductible:

Amount the policyholder needs to pay for covered health services before a health plan will begin to pay benefits. Usually a new deductible is met each calendar year.

EOB (Explanation of Benefits):

A detailed explanation from the insurance company that identifies the amount due for services provided. This includes any payments made by the insurance company and any listed co-payment, coinsurance, or deductible due from the policyholder.

Guarantor:

The person responsible for paying the bill.

Payment Arrangements:

A formal payment plan set up between a patient and our office when payment cannot be made in full.

Primary Insurance:

Designation given to the insurer that your claim will be submitted to first, for payment of services you received. For dependent children, the primary insurance is the parent with the first birthday of the calendar year. For example, if Dad’s birthday is July 1972 and Mom’s is January 1973, Mom’s birthday is first and would be the primary insurance. See also "Birthday Rule".

Prior Authorization/Pre-Certification:

A formal approval obtained from the insurance company prior to delivery of medical services. Many insurance companies require prior authorization or pre-certification for specific medical services, procedures or medications.

Subscriber:

The person who holds and/or is responsible for the medical insurance policy.

Secondary Insurance:

Designation given to the insurer that your claim will be submitted to second, for payment of services you received. See also "Birthday Rule."

Billing

Coding — how medical offices talk to insurance companies

Virtually every doctor who accepts health insurance uses codes (called CPT codes) that are assigned to every task they and their staff performs. Everything from a simple blood draw, to immunizations, to the ear check, to specimen handling — all these things are “coded” separately.

We use these standard billing codes to tell your insurance company what we have done at a visit. We also submit charges associated with various codes. The insurance company adjusts the portions that they cover and what they expect you to pay as well as what they expect us to write off based on contracts.

Any bill you receive from us is sent after the insurance adjustments have been made and reflect what your insurance company expects you to pay.

How does medical coding work?

The codes we use are to communicate with the the patient’s health insurance company to determine the payment amount that the doctor will receive for his or her services. Each diagnosis, procedure, survey, vaccine, and other service is assigned a code.

The medical office does not choose their own codes. They are standardized among all medical clinics.

The health insurance company wants to see what was done during a patient’s appointment. Hence, everything the doctor and the staff does has a code. If we fail to code for each issue addressed or every task completed we risk failing to meet metrics set by regulatory boards. This is why we can't simply do a procedure and not bill for it.

For example, if you are coming in for a child’s well visit, the pediatrician will submit a "claim" to the insurance company using the following codes:

- Established Well Visit – 99392

- Developmental Testing – 96110

- Hemoglobin – 85018

- Finger stick – 36416

- Lead Testing – 83655

- Hearing Screen – 92587

If the child gets immunizations, those have codes too:

- Flu – 90660

- MMR - 90707

Vaccine administration also uses a distinct set of codes. To further complicate things, some vaccines have a single administration code used with them, and others have multiple administration codes for a single vaccine.

- Admin – 90460

- Admin – 90461

Sick and well codes are different

What happens when something is identified during a well visit that isn't a "well" issue, such as an ear infection? Or what if you ask us to treat the wart or refer to physical therapy for that knee that's been an issue for months?

This question requires the the physician or nurse practitioner to perform an entirely different assessment than the well visit the child was getting.

In order to show the insurance company that a completely different assessment was done, codes are used for those diagnoses and a "sick" visit code is added to the "well visit" code.

But I have insurance, why do I have to pay?

Parents often think when they are looking at the bill that the doctor is nickel-and-diming parents, when in reality, it is the insurance company that requires us to show their work in this matter.

The insurance company decides what portion they will pay and what is reasonable but they will have the family pay.

It is the same as going to the restaurant and getting billed for all the side and extra orders. Although the main meal is accompanied by other things, like french fries or a salad, refills, side orders, substitutions and additions to the order are billed as extra. Only it's tricky because no one knows if the insurance company will pay for the sides or if they will require a family to pay for it.

Health care services are a la carte as well

Why do patients have balances if insurance ought to have paid?

The insurance policy may not pay for all the services performed. So when the billing staff submits a claim for a visit, the health insurance company often comes back and says, "We are not responsible for these codes/services; these are the member's responsibility per the member's health insurance policy.”

For example, the health insurance company may say, the policy your patient chose pays for a vision screen, but not for a hearing screen. Or they may say, we cover the well visit code, but not the ADHD code at the same time as the wellness visit.

It's not that we coded wrong (usually)

We often hear from parents who call to say that they talked to their insurance about a charge and were told that we used the wrong code.

Typically this means that we did a service or ordered labs with a code that is not covered. The insurance complany typically leaves it that we used the wrong code, but rarely offers up which code they will cover.

We can try to change the code to something else that the insurance company might cover, but unless they say which code we should use, it can be a futile game of trial and error.

For example, if we order labs for an obese child to make sure they aren't at increased risk because of high cholesterol, fatty liver, or diabetes, we use a diagnosis code for obesity to explain why the labs are necessary.

If the lab fee is denied by insurance, the parent will get a bill from the laboratory used. (This isn't even Pediatric Partner's bill, since we did not do the lab, but if we pick the right code, maybe insurance will pay for the laboratory fee that is certainly recommended for health risks.) We must change the code so and notify the laboratory so they can resubmit it to the insurance and hope for payment.

We might try any of the following if they apply:

- E66 for obesity (from experience, this is not paid, so we don't use it)

- Z68.54 BMI, pediatric, greater than or equal to 95th percentile for age (typically what we use on the initial lab order)

- L83 if a patient has Acanthosis nigricans (a skin darkening on skin folds of the neck, often associated with obesity)

If labs were abnormal, we could add the abnormal code, such as "elevated liver enzymes" or "hypercholesterolemia". We can't use these codes initially if it's only a screening because we won't know if we don't test.

Sometimes we resubmit different codes several times before finding the "right" one. (Note, the right one changes from insurance company to insurance company and even year to year within a company.)

What if we just don't address the extra stuff?

One option to avoid getting a bill for extra things covered at well visits is to have you come back later.

If we ONLY do well visit things at the well visit, it is more likely (though not guaranteed) that you will not get a bill. Most of the things recommended in Bright Futures are covered by insurance.

The "sick" visit issues are never part of a well visit. These might include ear infections, warts, and medication refills for asthma or ADHD. To correctly address and document these, we need to enter it into our charts, which generates codes. Sick visits typically incur a co pay, unlike well visits. So you might have a co pay for the visit added, whether your appointment was scheduled as a sick visit or a well visit, if sick topics are addressed.

So we can make it convenient and treat that ear infection we see, or refill your child's medications on the day of your well visit. Or we can ask that you reschedule for another day to address the non-well things.

Sometimes the line is very fuzzy.

Part of a well visit includes depression screens for adolescents. If it identifies depression, it would be poor care to push that to another day. But discussing depression is not a quick add on to a well visit. It deserves time. We deserve to be paid for our time.

By treating additional questions during a wellness visit, the doctor runs the risk of not being paid despite doing the work. On the other hand, not addressing the issues, the doctor runs the risk of upsetting the parent, who will probably think the doc is trying to squeeze another $30 copayment; which is clearly not the case.

Transparency is lost

One of the major problem with this is that patients don’t understand what they are financially responsible for. Sadly we as medical professionals often don't know either - there are too many companies that are not transparent in their process.

Just like with anything else, you get what you pay for. But patients overlook this issue when purchasing health insurance. They only look at the monthly premiums and chose the lowest one. But by doing that, they are often reducing the amount of coverage, which means patients will get stuck with larger portions of their medical bills.

Growing trend to save cost

The health insurance companies, in an effort to keep their premiums low, have shifted the cost to customers and their doctors. While in the past health insurance company’s may have covered 100%, now they are reducing the monthly premiums but only covering 70% of one’s medical expense. Hence all high deductible plans out there.

Why wasn't I told the insurance doesn't cover this?

There are virtually thousands and thousands of different health plans. We even have patients whose parents work for the same company, but have different insurance plan details with the same appearing insurance card.

We don’t have enough manpower or time to sit on the phone verifying every single patient’s healthcare coverage - especially for the additional things added in during a visit. We cannot know that your child will need a breathing treatment when you schedule to be seen for a cough or that your well visit will identify an ear infection in your baby or depression in your teen.

As a practice we believe it is the patient's responsibility to find out what is covered and what is not covered. The more time we spend on the phone with a patient's insurance company, the less time we are able to spend providing health care for our patients. We recognize the futility of this though. We know that you will not get the answers you need from your insurance company - even HR managers struggle to get real answers - and they have connections!

It all comes down to the best care

As a practice, we consider that treating patients based on what the insurance covers and what it doesn't, instead of treating by what the patient actually needs, is an unethical way to practice medicine.

Although most doctors will take into consideration health insurance stipulations, they will not compromise a child’s health as a result of health insurance restriction and cheap health insurance coverage plans.

If you have remaining questions, or don’t understand your medical bills, feel free to call our billing office.

Patient Responsibility and Billing

The medical industry is different from most because we do not bill our customers directly. We contract with insurance companies, who pay us what they feel is the amount due for certain services. They also have contracts with their policy holders, which describe the payment responsibility for the patient. We cannot alter the contract between a patient and their insurance company. In fact, we do not know what the specifics are between a policy holder and their insurance company. Each contract is different, even with the same insurance company. For example, Blue Cross Blue Shield (BCBS) policies with different companies and with individual plans are different from other BCBS policies, even if they are both PPO or HMOs. There are hundreds of various BCBS policies and each covers different services at various levels. We cannot know what is covered, what is considered not covered at all, or what is considered patient responsibility until we receive payment for services from the company.

We have attempted to discuss our policies on our website so that all patient families can know what our policies are, but we cannot list all covered or non-covered benefits because that is dependent on the contract between you and your insurance company. Please read your policies and ask questions to your insurance company before visiting the doctor so you know your financial responsibility.

We follow strict coding rules and cannot upcode or downcode without breaking the law. This means that a provider should use codes assigned to various sick and well diagnoses and level of difficulty of a visit. Our electronic medical record helps to properly assign codes to visits, which is one reason there is a push by the government to get more physicians on electronic medical records.

One major issue we are seeing is that insurance companies are not all covering separate issues when seen on the same date of service. Pediatric Partners follows the use of CPT as published by the American Medical Association. These CPT codes allow for the use of what is called Modifier -25 to identify separate preventive medicine service (well child exam) and a problem-oriented service (ear infection, hurt foot, earwax removal, etc) on the same date of service.

CPT is very clear on this point. In the guidelines preceding the Preventive Medicine Services codes, CPT states:

“If an abnormality/ies is encountered or a pre-existing problem is addressed in the process of performing this preventive medicine evaluation and management service, and if the problem/abnormality is significant enough to require additional work to perform the key components of a problem-oriented E/M service, then the appropriate office/outpatient code 99201-99215 should also be reported. Modifier -25 should be added to the office/outpatient code to indicate that a significant, separately identifiable evaluation and management service was provided by the same physician on the same day as the preventive medicine service. The appropriate preventive medicine service is additionally reported."

Some insurance companies argue that if they were to follow these CPT guidelines, physicians would game the system and would more often than not find a medical problem that would enable them to bill for both services, so they simply do not follow the guidelines at times.

We argue that our primary motivation in this situation is to avoid inconveniencing patients who present with acute problems at a preventive care visit. Rather than asking them to return on another date to divide the services, we perform both and submit a claim for both. We realize that this might take a few extra unscheduled minutes of our time, which can affect our office flow, but feel that it overall benefits families because a little longer wait time to avoid coming for multiple visits is preferable to most. Insurance companies handle this situation of addressing multiple issues on the same date differently. If payment for the second service is denied, we write it off, since physicians are usually prohibited under contract from balance billing the patient. If the insurance company says the payment is patient responsibility, it is insurance fraud for us to write off this charge. Many families are upset with us when we do not write things off for them, but we simply cannot by law.

A new twist in the use of the Modifier -25 is that insurance companies are putting this cost to the consumer, which is what leads to many billing questions. The extra cost often includes a second co-pay on the same day of service, since multiple issues were covered on that date. Please understand that it is your insurance contract that requires you to pay this portion, not our office specifically. Again, it would be insurance fraud for us to write off this portion of the charge, so we will not.

Unfortunately, because of your insurer's payment policy, in some cases we may have to complete your wellness care and your illness care in two separate visits to allow appropriate billing. If you have a health problem you want to discuss with your doctor during your well visit, the doctor may decide to treat that problem and ask you to schedule another appointment for your well visit. If the additional concerns are not urgent, you will be asked to schedule a separate visit to have that problem addressed.

Please understand that we will work with you to the extent that our contracts allow, but we are also a business and in these tough economic times we must be able to cover our increasing costs. Our rent increases yearly, our office staff and nurses salaries increase yearly. Vaccine costs are outpacing reimbursement rates. Malpractice costs are climbing. Costs to buy and maintain our electronic medical record and website to best serve our patients are substantial — a major reason that few physician offices have electronic medical records.

We would like to provide the best care to our patients in a timely and economical manner, but because of many issues, we may have to have you return for separate visits for each separate issue. We hope that this improves patient care, waiting times, and family understanding of billing practices.